install.packages(c("marginaleffects", "janitor", "ggdist"))Session 7: Using Observational Data to Estimate Causal Effects

We want to understand what factors make certain outcomes more likely to occur. What makes an individual more likely to vote in an election? What makes a country on the brink of democracy more likely to slide back into authoritarianism? What makes war between two countries more likely to break out?

We can use empirical research to help us discover what characteristics or features of our political actors or the environment in which they operate make these outcomes more likely to occur. Does election day registration increase the likelihood an individual will vote in an election? Does a free press make democratic backsliding less likely to occur? Do trade links reduce the likelihood two countries go to war with one another?

Many of the questions we ask cannot be answered using experiments. We are left, instead, to look back at the history of our outcome of interest (for example, global conflicts, democratic backsliding, elections), and attempt to tease out the role various factors played in shaping those outcomes. This section focuses on developing your ability to do this.

Set up

To complete this session, you need to load in the following R packages:

Install packages

To install new R packages, run the following (excluding the packages you have already installed):

You will also need to install an R package I built: polisciols. This package contains data published by some wonderful political scientists. You can read more about it in the package documentation.

This package is not published on CRAN1, so you will need to install it using the following code:

install.packages("devtools")

devtools::install_github("hgoers/polisciols")Remember, you only need to do this once on your computer. Run this in the console.

The economic benefits of justice

Appel and Loyle (2012) (two wonderful UMD alumni) explore the determinants of foreign direct investment (FDI) flows into and out of post-conflict states. States that are emerging from civil war often have an acute need for foreign and stable sources of capital. However, multinational corporations and other foreign commercial actors are likely to view post-conflict states as high risk countries in which to invest: the risk of a return to violence and instability is often high in the immediate aftermath of a civil war. Understanding this, leaders of post-conflict states often attempt to decrease this perceived risk.

Appel and Loyle argue that leaders can successfully do this by establishing post-conflict justice (PCJ) institutions. These institutions impose both domestic and reputational costs on post-conflict leaders. These costs allow leaders to signal their commitment to minimizing the risk of a return to violence and instability to foreign commercial actors. This is a great paper and I highly encourage you to take a look at their argument in detail.

Their argument focuses on leaders’ attempts to change foreign commercial actors’ perceptions of the risk of a return to violence. We cannot directly observe these commercial actors’ perceptions. However, we can observe the outcome of these perceptions: investment. Firms that have the means and desire to invest in a post-conflict country will make an assessment of the risk to their investment before committing the capital required to set up shop. If they believe the country is highly likely to return to conflict, they will not invest in it. If, on the other hand, they believe the risk of recidivism is low, they will invest.

If Appel and Loyle’s argument is correct, we should observe higher levels of FDI investment coming into post-conflict states that establish PCJ institutions compared to those that do not. PCJ institutions reduce the risk of a return to violence, which should - in turn - reduce firms’ beliefs about this risk. Firms invest when they believe the risk of a return to conflict to be low.

Appel and Loyle find strong evidence of this occuring. We will replicate and modify this empirical work. In doing so, we will become more familiar with the underlying mechanics of linear regression and strengthen our ability to interpret these models.

Let’s get started!

Net FDI inflows to post-conflict states

Appel and Loyle provide us with data on 95 different post-conflict states. These include all states that had internal armed conflicts, including internationalized conflicts, that resulted in at least 25 battle-related deaths and were settled between 1970 and 2001.

We can access these data through polisciols::ebj:

head(ebj) id ccode country_name pcj net_fdi_inflows gdp_per_capita

1 71 41 Haiti No institutions -9.8000 1182.498

2 71 41 Haiti No institutions 6.6000 1088.680

3 154 52 Trinidad & Tobago No institutions 510.1589 7742.736

4 102 70 Mexico No institutions -340.6904 6894.704

5 102 70 Mexico No institutions 6460.7998 7780.053

6 67 90 Guatemala PCJ institutions 431.3800 3061.873

gdp gdp_per_capita_growth ex_rate_fluc cap_account_openness labor

1 8407079981 -2.1324685 0.000000 -0.7681904 68.5

2 8055393763 -14.8832922 1.776603 -0.0871520 67.9

3 9542938026 1.9370972 0.000000 -1.1305820 55.2

4 628418000000 -7.8634830 1.978028 1.1804080 59.8

5 730752000000 5.2345648 1.129686 1.1804080 61.3

6 31339424077 0.6277104 1.046489 1.2642760 63.1

f_life_exp polity2 pol_constraints conflict_duration damage

1 55.02233 7 0.00 1 0.000000

2 56.09750 -7 0.00 1 12.855902

3 72.61483 9 0.84 1 -2.787351

4 74.67104 4 0.39 1 0.000000

5 75.23493 6 0.39 1 -8.949999

6 67.46067 8 0.43 31 -43.714600

peace_agreement victory cold_war

1 No agreement Victory Post-Cold War

2 No agreement Victory Post-Cold War

3 No agreement Victory Post-Cold War

4 Peace agreement No victory Post-Cold War

5 No agreement No victory Post-Cold War

6 Peace agreement No victory Post-Cold WarThey focus on the 10-year period immediately following the conflict’s conclusion. This is the period in which we would expect foreign commercial actors to perceive the risk of a return to violence and instability to be greatest and, therefore, the period in which leaders’ attempts to quash these perceptions to be most relevant.

Each row in this data set represents a single post-conflict state. The data provided are a summary of the 10-years post-conflict. For example, net_fdi_inflows provides us with the total net FDI inflows (dollar amount invested in the country minus the dollar amount divested from the country) each post-conflict state received across the whole 10-year period.

Tip

You can learn more about each variable using the following command:

?ebjTheir outcome of interest is net FDI inflows. Remember, if their argument is correct we would expect post-conflict states that have established a PCJ institution to have higher net FDI inflows than than states that did not. Let’s take a look at those net inflows:

summary(ebj$net_fdi_inflows) Min. 1st Qu. Median Mean 3rd Qu. Max.

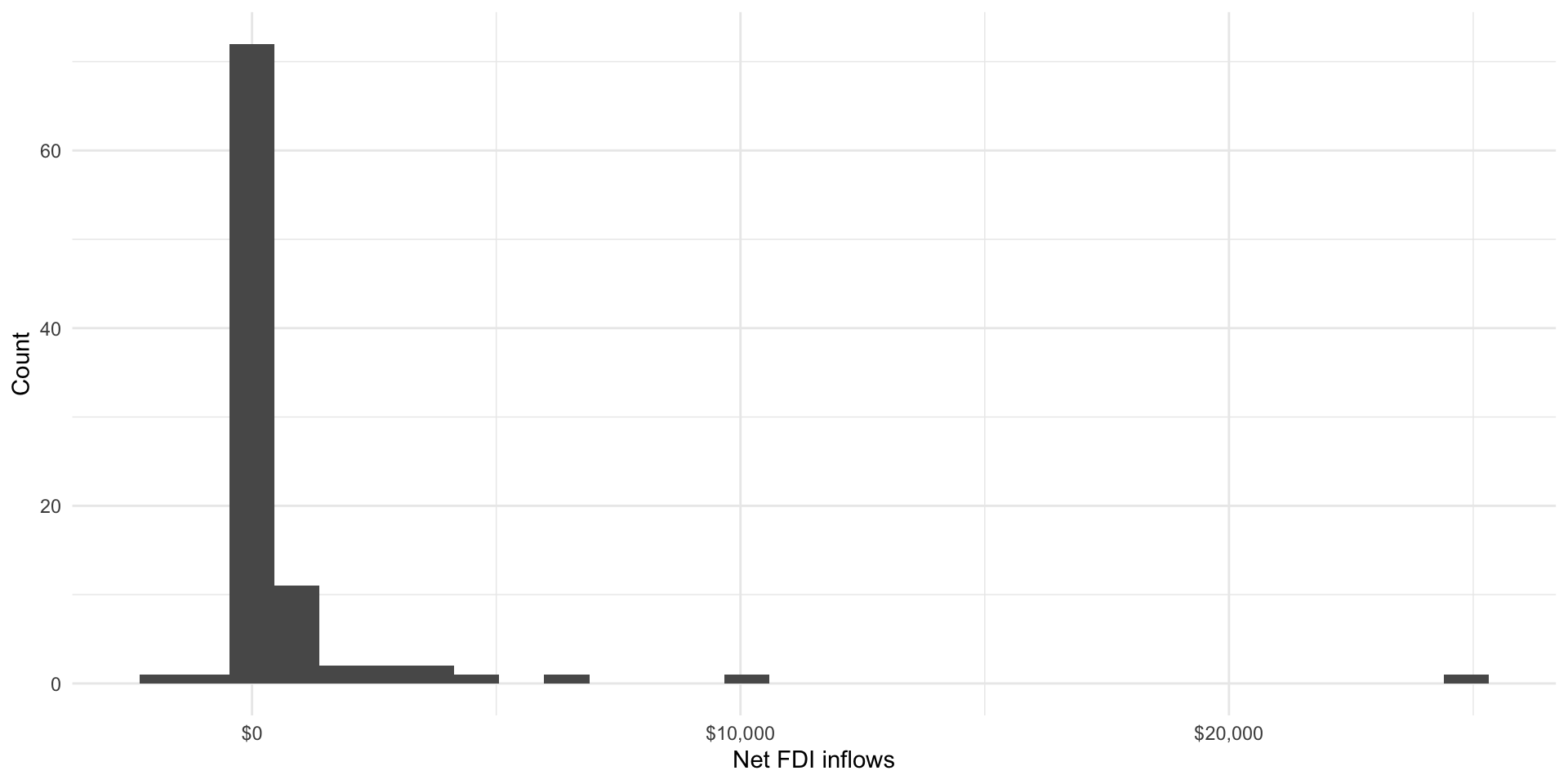

-1858.914 -0.572 38.290 759.146 408.250 24836.787 ggplot(ebj, aes(x = net_fdi_inflows)) +

geom_histogram() +

theme_minimal() +

labs(x = "Net FDI inflows",

y = "Count") +

scale_x_continuous(labels = scales::dollar)

On average, post-conflict countries received $759.15 million in net FDI inflow. So, countries in our sample tended to receive more investment than they lost in the 10-year period following the end of their conflict.

Looking at the histogram above we can see that this average is not a particularly good summary of our data: the majority of countries received a smaller amount of net FDI inflows. The peak the distribution is sitting closer to $0. Looking at the five number summary printed above the histogram we can see that 50 percent of the countries in our sample received between -$0.57 and $408.25 million in net inflows.

Note

The middle 50 percent of a vector of numbers sits between the first quartile (below which 25 percent of those numbers fall) and the third quartile (below which 75 percent of those numbers fall). To illustrate, consider the following:

Why is our average sitting so far above where the majority of the countries’ net FDI inflows fell? There appears to be a clear outlier in our data: Russia received a net FDI inflow of $24,836.79 million in the 10 years following the end of the First Chechen War in 1997. You can see that this is pulling the average net FDI inflows up well above the median inflow across our group of post-conflict states. Keep this in mind, because we will return to it later in the course.

PCJ institutions

Appel and Loyle ask whether states that have PCJ institutions successfully attract greater net FDI inflows than those that do not. Therefore, their main explanatory variable is the existence of PCJ institutions.

In their dataset the variable pcj indicates whether the the state established a PCJ institution within five years following the end of the conflict. What proportion of states did this?

tabyl(ebj, pcj) pcj n percent

No institutions 77 0.8105263

PCJ institutions 18 0.1894737The majority of post-conflict states did not establish any PCJ institutions in the five years proceeding the end of their conflicts.

Relationship between PCJ institutions and net FDI inflows

Of the states that do have a PCJ institution, do they tend to receive higher net FDI inflows than their less reconciliatory counterparts?

# A tibble: 2 × 2

pcj avg_net_fdi

<fct> <dbl>

1 No institutions 425.

2 PCJ institutions 2189.Yes! On average, states that established a PCJ institution received higher net FDI inflows than those states that did not. This difference looks large. It’s $1,763.52 million in net inflows.

Ready for something very cool? At the end of the day, OLS regression is just fancy averaging. Let’s fit a linear regression model to these data and look at the results:

m <- lm(net_fdi_inflows ~ pcj, data = ebj)

modelsummary(m,

statistic = NULL,

coef_rename = c("pcjPCJ institutions" = "PCJ institutions established"))| (1) | |

|---|---|

| (Intercept) | 425.006 |

| PCJ institutions established | 1763.517 |

| Num.Obs. | 95 |

| R2 | 0.057 |

| R2 Adj. | 0.047 |

| AIC | 1784.5 |

| BIC | 1792.2 |

| Log.Lik. | -889.253 |

| F | 5.618 |

| RMSE | 2811.91 |

We get the same numbers as above! Take a minute to interpret the intercept and coefficient estimate yourself. Can you see the connection to our simple grouped averages above?

Check your answer

The intercept is the predicted value of our outcome variable when all independent variables are equal to zero. Here, we have one independent variable which is equal to zero when the country did not establish PCJ institutions. Our model predicts that post-conflict countries without PCJ institutions will have the net FDI inflow that post-conflict countries in our sample without PCJ institutions had on average.

The coefficient estimate is the predicted average difference in the outcome following a one-unit change in the independent variable. Here, a one-unit change in our independent variable is a move from no PCJ institutions (where pcj = 0) to at least one PCJ institution (where pcj = 1). Our model predicts that post-conflict countries with PCJ institutions will have on average $1,763.52 million more in net FDI inflows because this is the difference between the average net inflows of countries in our sample without PCJ institutions and those with them.

According to this model, what is the average predicted net FDI inflows for countries that did not establish PCJ institution?

Answer

Post-conflict states that did not establish a PCJ institution received, on average, net FDI inflows of $425.01 million in the 10-year period after conflict.

To get this, I looked at the intercept coefficient which tells us the average predicted value of our outcome variable when all explanatory variables are equal to zero or their baseline category.

According to this model, what is the average predicted net FDI inflows for countries that did establish PCJ institution?

Answer

In contrast, states that did establish PCJ institution received, on average, net FDI inflows of $2,188.52 million.

In other words:

\[ Average\ net\ FDI\ inflows = \beta_0 + \beta_1 Institution\ established + \epsilon \]

When an institution was established (i.e. \(Institution\ established = 1\)):

\[ Average\ net\ FDI\ inflows = 425.01 + 1763.52 * 1 + \epsilon \\ \]

\[ Average\ net\ FDI\ inflows = 2188.52 \]

Substantive significance

So, we found support for Appel and Loyal’s hypothesis: countries that established PCJ institutions within the first five-years after conflict received more net FDI inflows than those that did not establish these institutions. But, was this difference large? These institutions impose real costs on post-conflict leaders. Is the predicted boost in net FDI inflows generally worth this cost? More generally, is this difference substantively significant?

Note

Substantive significance is different from statistical significance, which we will discuss in detail in our last session. Here, we are interested in whether the difference is large enough for our political actors to care about it.

To illustrate, imagine if I told you that studying this course material for an additional five hours would lead to a one-point increase in your quiz mark. I’m not sure many of you would put in that additional work for such a small reward. If, on the other hand, I told you that it would boost your mark by 15 points, you might be more willing to spend your afternoon with these materials.

There is no one right or wrong answer to the question of substantive significance. For example, perhaps someone who is one point away from a perfect grade would be willing to put in the extra hours to secure that one additional mark. Substantive significance rests much more on your argument for it, rather than a hard-and-fast threshold that must be reached (which is the case for statistical significance).

I argue that this finding is substantively significant. These countries are recovering from conflict: their economies are generally very weak. Leaders are often very keen to find stable and reliable sources of funding to promote and strengthen their battered economies. This average difference of $1,763.52 million is; therefore, likely to incentivize this policy.

But what about other factors that shape net FDI inflows?

One of Appel and Loyle’s major contributions is their critique of approaches to estimating net FDI inflows that focus only on economic factors. They argue that there are several political factors that are significant determinants of other countries’ and foreign firms’ willingness to invest in these war-torn countries.

This critique is very valid, but it suggests that there are many different things influencing this outcome of interest, including economic factors. We have only looked at the political! The economists might turn around and accuse us of doing the very thing Appel and Loyle accused them of!

Let’s add some of those economic factors into our model. We will start with an intuitive one: individuals’ economic wealth (measured as GDP per capita). I expect that foreign firms will be more willing to invest larger sums of money into economies with richer citizens. These citizens will be more willing and able to purchase the goods and services provided by those firms.

Therefore, I hypothesize that the greater a state’s GDP per capita, the larger its net FDI inflows. I expect this to be the case regardless of whether the state has established a PCJ institution. Let’s test this claim:

m <- lm(net_fdi_inflows ~ pcj + gdp_per_capita, data = ebj)

modelsummary(m,

statistic = NULL,

coef_rename = c("pcjPCJ institutions" = "PCJ institutions established",

"gdp_per_capita" = "GDP per capita (current USD)"))| (1) | |

|---|---|

| (Intercept) | -319.173 |

| PCJ institutions established | 1673.288 |

| GDP per capita (current USD) | 0.318 |

| Num.Obs. | 95 |

| R2 | 0.142 |

| R2 Adj. | 0.124 |

| AIC | 1777.5 |

| BIC | 1787.7 |

| Log.Lik. | -884.742 |

| F | 7.638 |

| RMSE | 2681.52 |

We continue to find a positive relationship between net FDI inflows and the establishment of a PCJ institution. In other words, countries that established PCJ institutions received, on average, larger net FDI inflows than those that did not establish these institutions. Additionally, we can now state that this is the case regardless of how rich or poor individuals within the country are.

We do this by holding constant the other variables in the model. This can be a little tricky to wrap your head around, so please be patient with yourselves. When we introduce multiple variables into our linear regression models we move from a line of best fit to a plane of best fit. You add an additional dimension to your plane for each additional variable you include in your model. To illustrate, look at the model we just fit (which has two variables) plotted against the observed values for whether the country had a PCJ institution, its GDP per capita, and the net FDI inflow it received:

Show the code

# You can produce interactive graphs in R using `plotly`. This is a bit beyond

# the R code you have been introduced to thus far, but if you are interested in

# learning more check out the `plotly` documentation.

library(plotly)

# Get all plotted points for PCJ

points_pcj <- ebj |>

distinct(pcj) |>

pull()

# Get all plotted points for GDP per capita

points_gdp <- seq(min(ebj$gdp_per_capita, na.rm = T),

max(ebj$gdp_per_capita, na.rm = T),

by = 1)

# Get the predicted values for net FDI inflows from the model

new_df <- crossing(

gdp_per_capita = points_gdp,

pcj = points_pcj

)

pred_values <- augment(m, newdata = new_df) |>

pull(.fitted)

pred_values_matrix <- matrix(pred_values, nrow = length(points_pcj), ncol = length(points_gdp))

# Plot the plane

plot_ly() |>

add_surface(x = points_gdp,

y = points_pcj,

z = pred_values_matrix,

colors = "pink") |>

add_markers(x = ebj$gdp_per_capita,

y = ebj$pcj,

z = ebj$net_fdi_inflows,

type = "scatter3d",

alpha = 0.75) |>

layout(showlegend = FALSE)

Note

This graph is interactive. Have a play around with it.

Our model is no longer the line of best fit. It is now the linear plane of best fit. For any given value of GDP per capita and whether the country has PCJ institutions or not, we have a predicted value of net FDI inflows. This predicted value is the value that minimizes the distance between itself and all the values of both GDP per capita and whether the country has a PCJ institution or not.

Interpreting multiple linear regression models

The intercept here is not informative on its own. It tells us the estimated average net FDI inflows for countries that do not have PCJ institutions (pcj = 0) and in which citizens had a GDP per capita of $0 (gdp_per_capita = 0). Although the majority of countries did not establish a PCJ institution, there are no countries in the world that have a GDP per capita of $0.

Let’s instead focus on the other coefficients. We find that states that established a PCJ institution received, on average, net FDI inflows of $1,673.29 million more than states that did not, holding that country’s GDP per capita constant. I have picked one value of GDP per capita and then calculated the difference between the predicted value of net FDI inflows for a countries with that GDP per capita and without PCJ institutions compared to that for a country with that GDP per capita and with PCJ institutions. The value of GDP per capita that you pick does not matter because this is a linear plane.

Note

To illustrate, say I pick a GDP per capita of $0. The predicted net FDI inflow for a country without a PCJ institution is therefore:

\[ Net\ inflow = -319 + \beta_{PCJ}(0) + \beta_{GDP\ per\ cap}(0) \\ Net\ inflow = -319 + 1673(0) + 0.318(0) \\ Net\ inflow = -319 \]

The predicted net FDI inflow for a country with a PCJ institution (and a GDP per capita of $0) is:

\[ Net\ inflow = -319 + \beta_{PCJ}(1) + \beta_{GDP\ per\ cap}(0) \\ Net\ inflow = -319 + 1673(1) + 0.318(0) Net\ inflow = 1354 \]

The difference is $1673 (the coefficient for the PCJ variable).

I can do the same calculations for a country with a GDP per capita of $25,000. Here is the predicted net FDI inflow for a country without PCJ institutions:

\[ Net\ inflow = -319 + 1673(0) + 0.318(25000) \\ Net\ inflow = 7631 \]

And for a country with PCJ institutions:

\[ Net\ inflow = -319 + 1673(1) + 0.318(25000) \\ Net\ inflow = 9304 \]

Again, the difference is $1673 (the coefficient for the PCJ variable).

We also find that an increase in the GDP per capita of a state of $1,000 is associated with an increase of $318.45 million in net FDI inflow, on average and holding whether they have PCJ institutions constant. This is consistent with our expectations that, holding all else constant, a country with a richer population is a more attractive investment destination than a country that has poorer citizens.

Using this richer model

We now have a richer understanding of the determinants of net FDI inflows to post-conflict countries. We have accounted for both economic and political determinants of those flows. Although it is often useful to look at the estimated relationship of each of those variables individually (as we did just above), we often learn more by looking at the whole model in context.

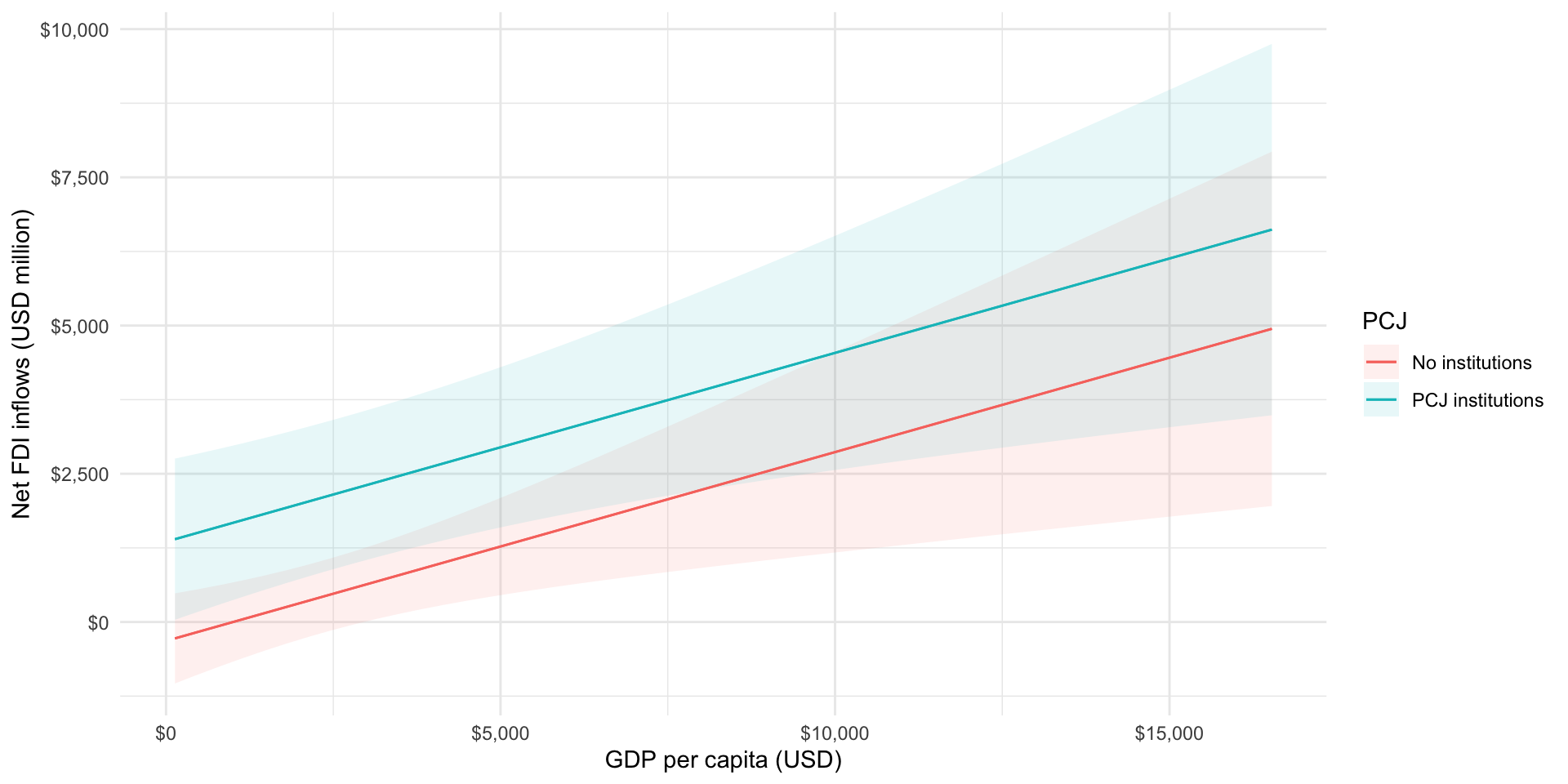

As usual, one of the easiest ways to communicate this is through a visualization. Let’s look at the predicted net FDI inflows for post-conflict countries that established and did not establish PCJ institutions across a range of plausible GDP per capita values:

plot_predictions(m, condition = c("gdp_per_capita", "pcj")) +

labs(x = "GDP per capita (USD)",

y = "Net FDI inflows (USD million)",

color = "PCJ",

fill = "PCJ") +

scale_y_continuous(labels = scales::dollar) +

scale_x_continuous(labels = scales::dollar) +

theme_minimal()

We can see that countries with PCJ institutions (represented by the blue line) are predicted to have more net FDI inflows than countries without these institutions (represented by the red line) across all values of GDP per capita. Because the model is linear, the distance between the red and blue lines is constant across all values of GDP per capita.

Note

The coloured bands around the line showing the predicted values of net FDI inflows are the confidence intervals. We will discuss these more in later sessions.

The full model

Appel and Loyle control for many more economic and political factors shaping net FDI inflows. Remember, they are arguing that the extensive literature that looks at the determinants of FDI flows to post-conflict states failed to account for this important political factor. However, that same literature did a very good job of identifying the economic factors, including countries’ economic development, size, and growth rates, that shape this outcome. They don’t dispute that these factors are also important, they just argue that we should also think about the role PCJ institutions play in shaping foreign firms’ beliefs about the risk of returning to violence.

So, let’s account for these other factors:

m <- lm(net_fdi_inflows ~ pcj + gdp_per_capita + gdp + gdp_per_capita_growth +

cap_account_openness + ex_rate_fluc + labor + f_life_exp +

pol_constraints + polity2 + damage + conflict_duration + peace_agreement +

victory + cold_war,

data = ebj)

modelsummary(m,

statistic = NULL,

coef_rename = c("pcjPCJ institutions" = "PCJ institutions established",

"gdp_per_capita" = "GDP per capita (current USD)",

"gdp" = "GDP (current USD)",

"gdp_per_capita_growth" = "GDP per capita growth rate (%)",

"cap_account_openness" = "Capital account openness",

"ex_rate_fluc" = "Exchange rate fluctuation",

"labor" = "Labor force participation (%)",

"f_life_exp" = "Average female life expectancy (years)",

"pol_constraints" = "Political constraints",

"polity2" = "Regime type (Polity score)",

"damage" = "Pre-conflict GDP lost",

"conflict_duration" = "Conflict duration (years)",

"peace_agreementPeace agreement" = "Peace agreement",

"victoryVictory" = "Decisive victory",

"cold_warCold War" = "Cold War"))| (1) | |

|---|---|

| (Intercept) | -1278.322 |

| PCJ institutions established | 1960.282 |

| GDP per capita (current USD) | -0.111 |

| GDP (current USD) | 0.000 |

| GDP per capita growth rate (%) | 37.400 |

| Capital account openness | 198.823 |

| Exchange rate fluctuation | -42.516 |

| Labor force participation (%) | 9.844 |

| Average female life expectancy (years) | 3.475 |

| Political constraints | 2557.954 |

| Regime type (Polity score) | -90.169 |

| Pre-conflict GDP lost | 28.379 |

| Conflict duration (years) | 0.811 |

| Peace agreement | -1215.137 |

| Decisive victory | -33.969 |

| Cold War | 81.531 |

| Num.Obs. | 95 |

| R2 | 0.514 |

| R2 Adj. | 0.422 |

| AIC | 1749.5 |

| BIC | 1792.9 |

| Log.Lik. | -857.752 |

| RMSE | 2018.34 |

Even when we account for all the political, economic, and conflict-related factors that the literature previously identified to be important, we still find that the existence of PCJ institution shapes the net FDI inflows of post-conflict states.

Including categorical variables with multiple categories

Appel and Loyle look at a number of political factors driving net FDI inflows to post-conflict states. They include a measure of regime type: the country’s Polity score. This score measures a state’s regime type along a 21-point scale from -10 (perfect autocracy) to 10 (perfect democracy). Broadly speaking, political scientists have usefully broken this spectrum down into three regime types: democracies, hybrid regimes, and autocracies.

Let’s modify their measure of regime type to reflect these broad categories, instead of treating it as a continuous variable:

I have a theoretical reason to do this. I suspect that there is not a clear linear relationship between investors’ confidence in a post-conflict state and its regime type when we treat regime type as a continuous spectrum moving linearly from autocracies to democracies. In other words, I don’t think that moving one Polity score away from being an autocracy to being a democracy would have a consistent effect on investor confidence (and; therefore, net FDI inflows). Appel and Loyle’s model agrees with me: the regime type variable is not statistically significant.

Rather, I suspect that strong democracies and strong autocracies provide the political stability required to comfort foreign investors. These investors believe that the strong control democrats and autocrats have over their citizens and institutions reduces the risk that the country will re-enter into conflict. However, hybrid regimes do not tend to have this level of control. Investors are; therefore, less likely to invest in post-conflict countries with hybrid regimes.

Let’s test this!

We now have a categorical variable with three categories: democracy, hybrid regime, and autocracy. We have thus far largely dealt with binary categorical variables (voted or not, Southern or not, female or not). How do we use and interpret multiple categorical variables in regression analysis?

Happily, the intuition remains the same as with our binary categorical variables. We hold one category out as our baseline category and then compare the associated effects of the other categories to this one.

Let’s step through that using a stripped back version of our model:

m <- lm(net_fdi_inflows ~ pcj + regime_type, data = ebj)

modelsummary(m,

coef_rename = c("pcjPCJ institutions" = "PCJ institutions established",

"regime_typeDemocracy" = "Democracy",

"regime_typeHybrid regime" = "Hybrid"),

stars = T)| (1) | |

|---|---|

| + p | |

| (Intercept) | 214.555 |

| (497.984) | |

| PCJ institutions established | 1816.169* |

| (764.093) | |

| Hybrid | 553.893 |

| (667.644) | |

| Democracy | -148.124 |

| (809.623) | |

| Num.Obs. | 95 |

| R2 | 0.068 |

| R2 Adj. | 0.037 |

| AIC | 1787.4 |

| BIC | 1800.1 |

| Log.Lik. | -888.688 |

| F | 2.217 |

| RMSE | 2795.25 |

You’ll note that autocracies are missing from our regression table. This is because they are being held out as our baseline category. Their effect on net FDI inflows is captured by the intercept coefficient.

Tip

We often say that the intercept coefficient represents the predicted average value of our outcome of interest when all independent variables are set to zero. It might be useful for you to think of your baseline category as taking on the value zero. For example, we can think of autocracy = 0.

Our model suggests that autocracies (regime_type = "Autocracy") that have not established a commission (pcj = "No institutions") have a predicted average net FDI inflow of $214.55 million.

The coefficients on democracies and hybrid regimes need to be interpreted in relation to autocracies (their baseline category). From our model, we can see that the coefficient for democracies is negative and the coefficient for hybrid regimes is positive. That means that, on average, democracies tend to receive less net FDI inflows than autocracies and hybrid regimes tend to receive more net FDI inflows than autocracies, holding all else constant.

Predictions with multiple categorical variables

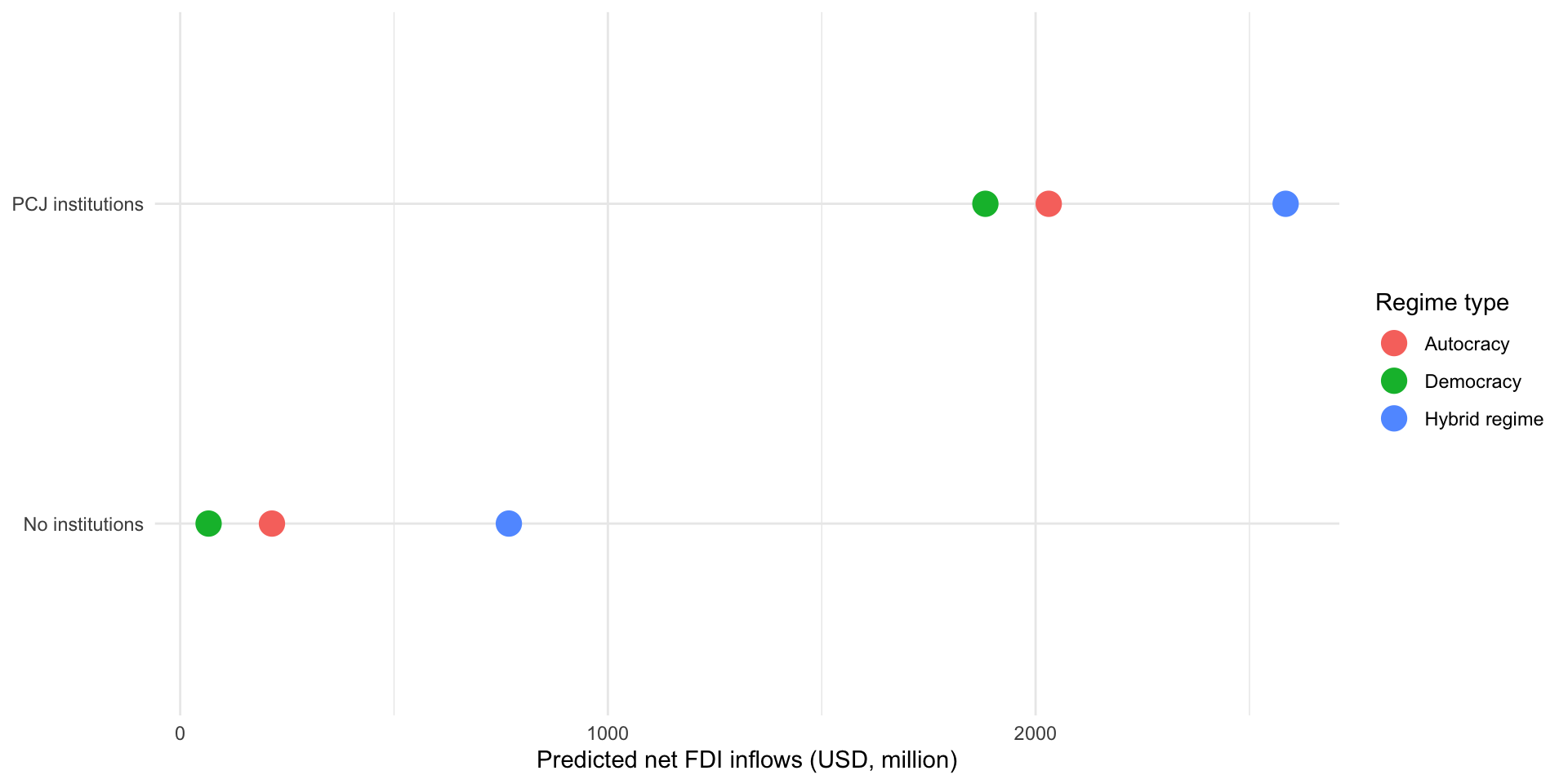

Using our model, what do we predict to be the net FDI inflows for democracies, autocracies, and hybrid regimes that either have a PCJ institutions or do not?

First, let’s create a table with each possible combination of these two variables of interest:

new_data <- tibble(pcj = factor(c("No institutions",

"PCJ institutions"))) |>

cross_join(

tibble(regime_type = factor(c("Autocracy", "Democracy", "Hybrid regime")))

)

new_data# A tibble: 6 × 2

pcj regime_type

<fct> <fct>

1 No institutions Autocracy

2 No institutions Democracy

3 No institutions Hybrid regime

4 PCJ institutions Autocracy

5 PCJ institutions Democracy

6 PCJ institutions Hybrid regimeThen we can use our model to predict what we expect a hypothetical state with each of these combinations of characteristics to receive in net FDI inflows:

pred <- augment(m, newdata = new_data)

pred# A tibble: 6 × 3

pcj regime_type .fitted

<fct> <fct> <dbl>

1 No institutions Autocracy 215.

2 No institutions Democracy 66.4

3 No institutions Hybrid regime 768.

4 PCJ institutions Autocracy 2031.

5 PCJ institutions Democracy 1883.

6 PCJ institutions Hybrid regime 2585. That’s a bit unweildy. Let’s visualize it!

ggplot(pred, aes(x = .fitted, y = pcj, colour = regime_type)) +

geom_point(size = 5) +

theme_minimal() +

labs(x = "Predicted net FDI inflows (USD, million)",

y = NULL,

colour = "Regime type")

We can clearly see that states that established PCJ institutions received, on average, larger net FDI inflows than states that did not, no matter their regime type. Further and completely counter to my hypothesis, hybrid regimes have, on average, the highest net FDI inflows compared to democracies and autocracies even when we account for whether the state has a PCJ institution.

I’m not too worried: none of these coefficients are anywhere close to being statistically significant. I suspect that there is a more complex relationship underlying commercial actors’ beliefs about the stability of hybrid regimes, democracies, and autocracies and its effect on net investment flows. But I hope this serves as a good illustration of how we can use multiple categorical variables in our analyses.

Quiz

Head over to ELMs to complete this session’s quiz. You need to score 80% on it to gain access to the next session’s quiz.

References

Appel, Benjamin J, and Cyanne E Loyle. 2012. “The Economic Benefits of Justice: Post-Conflict Justice and Foreign Direct Investment.” Journal of Peace Research 49 (5): 685–99. https://doi.org/10.1177/0022343312450044.

Footnotes

The Comprehensive R Archive Network (CRAN) hosts all R packages that can be installed easily using the familiar

install.packages()function. These packages have gone through a comprehensive quality assurance process. I wrotepolisciolsfor this class and update it regularly. I, therefore, will not host it through CRAN: the quality assurance process takes too long to be practical for our schedule. Instead, you are downloading it directly from its Github repository.↩︎